Rent A Room Relief 2017 18 Allowance

Grant Of Adhoc Relief Allowance 2018 10 Of Basic Pay Of The Civil Servants Of Balochistan Government Revision In The Rates Of Ho Allowance Government Grant

7th Pay Commission Fitment Factor And House Rent Allowance No Change Therein Is Envisaged Allowance Rent Paying

Pin On Income Tax

Pin On Microsoft Excel Accounting

Find Different Ways To Calculate Hra Income Tax Income Tax Return Online Taxes

Figuring Out Your Form W 4 Under The New Tax Law How Many Allowances Should You Claim In 2018 Pinterest Advice Allowance Form

How does it affect other reliefs and taxes.

Rent a room relief 2017 18 allowance. The 2017 to 2018 helpsheet has been added to this page. The helpsheet has been added for the tax year 2016 to 2017. A rent a room property business does not qualify for either partial relief or full relief under the property allowance. What conditions must be met.

In addition the property allowance is not available at all to an individual if they have a. If it does then you are taxed on the. Frank lets out the spare room in the home he owns for a rent of 200 a week giving him an annual income of 10 400 which is more than the rent a room allowance. The rent a room scheme lets you earn up to a threshold of 7 500 per year tax free from letting out furnished accommodation in your home.

If you let a room in your home the income you receive may be exempt from tax. 2016 to 2017 rent a room limit has been updated. For the tax year 2016 to 2017 the annual rent a room limit is 7 500. The income you receive must not exceed the exemption limit.

How is relief granted. Individuals who claim rent a room relief and have income from letting rooms for more than the current threshold will pay less tax as a result of this. What type of residence qualifies. 2018 to 2019.

2019 to 2020. As the rent a room relief limit currently 7 500 is more generous than the property allowance this is unlikely to be a concern. His tenant paid him gross rent of 13 000. 2017 to 2018.

He sub let a room during 2018. While the room was sub let john spent 1 500 on repairs on maintaining the let room. John qualifies for rent a room relief for 2018 as his gross income from letting the room did not exceed the 2018 limit 14 000. This reduces to 3 750 if someone else receives income from letting accommodation in the same property such as a joint owner.

If he stays in the rent a room scheme he will be taxed at his top rate of tax on the income above 7 500. Income of 1 000 or less either the income is exempt from income tax or the taxpayer can choose to disapply the allowance and calculate the profit or loss under normal business.

Pay Scale Revised Chart With Adhoc Relief Allowance 2020 In 2020 Education In Pakistan Chart Revision

Pay Scale Revised In Budget 2020 21 Chart Grade 1 To 21 Bise World Pakistani Education Entertainment In 2020 Salary Increase Salary Federal Employee

Pin On Income Tax

81v4ms3x22qccm

Income Tax Return Which Itr Should I File Income Tax Return Tax Return Income Tax

Rent A Room Scheme Making Money From Your Spare Room

A Little Boost Tax Adviser

How The New Tax Law Affects Rental Real Estate Owners Mitchell Wiggins

Uniform Tax Rebate Form P87 Download Tax Refund Tax Rebates

How To Check Income Tax Refund Status Online Income Tax Return Income Tax Tax Return

Notification House Rent Increase 2019 For Islamabad High Court Employees Education In Pakistan Islamabad Court

What Is The Rent A Room Scheme All You Need To Know

Section 24 Mortgage Interest Relief Optimise

Looking To Earn 14 000 Tax Free Get That Spare Room Ready

Increase Of House Rent Allowance In Salary For Sindh Employees Only Education In Pakistan Sindh Salary

11 Money Saving Tips I Used To Save 15 000 Last Year Money Saving Challenge Savings Challenge Money Plan

Small Business Loan Approvals Continue To Rise Says New Biz2credit Report Small Business Trends Small Business Lending Business

Notification Chief Justice Of The Supreme Court Special Judicial Allowance 2019 Notification No F 1 37 009 Sca Dated 16 Chief Justice Judicial Supreme Court

Education Posts Transfer As A Director Public Instruction Ee Punjab Notification No Soe1 1 44 2018 Dated Lah Elementary School Teacher Education Instruction

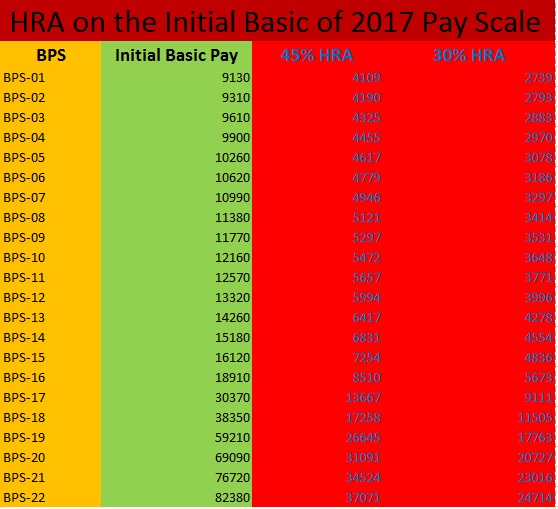

Classification Of Cities For Hra As Per 7th Cpc X Y Z Classification Of Cities For Hra 2020 Hra 7thcpc Hra2020 In 2020 Cpc Municipal Corporation Classification

Letting A Room Through Airbnb Hmrc Tracks Your Income Data The Tax Blog

2019 Income Tax Filing Tips And Free Tax Organizer Atkins E Corp Tax Organization Income Tax Preparation Income Tax

2019 Income Tax Filing Tips And Free Tax Organizer Atkins E Corp Tax Organization Income Tax Preparation Income Tax

News Archives Itechsoul Last Date Schemes Train

Taxation Rules For Landlords 2018 2019 Update Homelet

New Buy To Let Interest Relief Tax Changes Explained

Ato Reasonable Travel Allowances Atotaxrates Info

Uniform Tax Rebate Form P87 Download Tax Refund Tax Rebates

For Sale Sign On An Empty Piece Of Land Aff Sign Sale Empty Land Piece Ad How To Buy Land Plots For Sale Land For Sale

Https Taxscouts Com Calculator Rental Income Tax

Expected Increase House Rent Allowance In Budget 2018

Increase In House Rent Allowance Medical Allowance And 10 To 15 Pay

Tax Free Rental Income Up To 8 500

Pin By Samantha Begay On For The Home Chores For Kids Age Appropriate Chores Chore Chart Kids

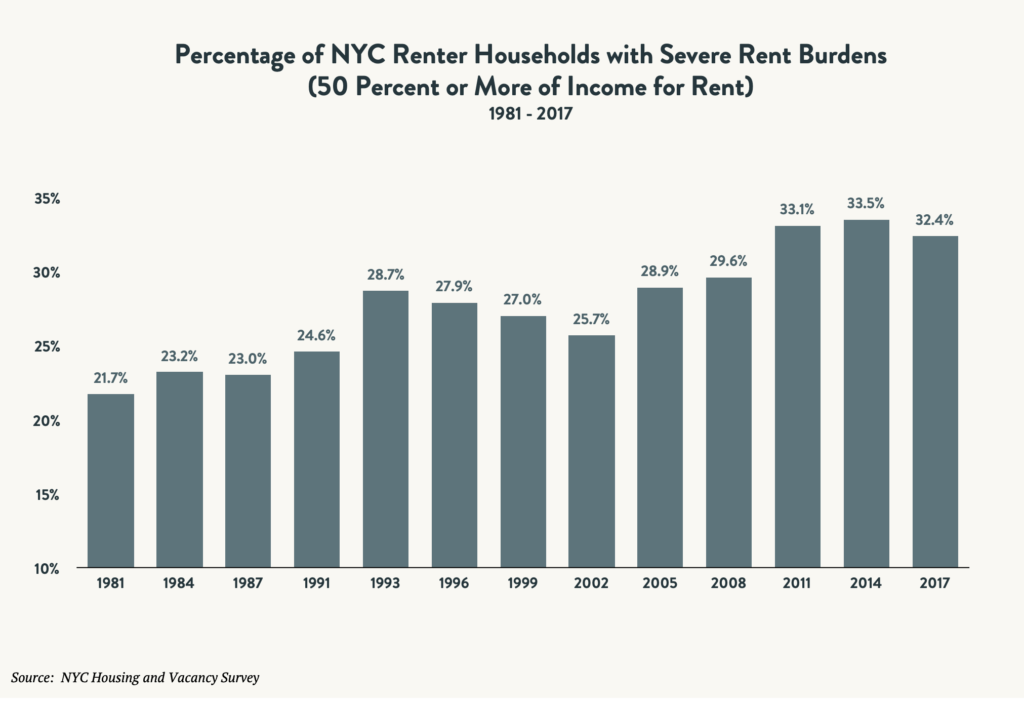

State Of The Homeless 2018 Coalition For The Homeless

Income From House Property Income Tax Deductions On Home Loans Property

Punjab Teacher Salary Calculator 2019 For The Month Of January Teacher Salary Salary Calculator Education In Pakistan

Https Www Facebook Com Photo Php Fbid 10158296442625831 In 2020

Section 80gg Deduction On Rent Paid

Publication 908 02 2020 Bankruptcy Tax Guide Internal Revenue Service

Freelance Videographer Contract Template Beautiful Sample Freelance Contract Templates Pages Wor In 2020 Freelance Graphic Design Contract Template Free Graphic Design

Personalized Chore Punch Cards Kids Rewards Chores For Kids Kids Behavior

Diy Clothespin Chore Chart Chore Chart Kids Charts For Kids Chores For Kids